Notes on RBC calibration

My notes on RBC calibration.

Read more about calibration

- Dynare’s manual

- Computational Methods for Economics

- Chad Fulton’s notes on RBC calibration

- Sims’ note

- Example by Joao Madeira

- ABCs of RBC, King and Rebelo (1999)

Baseline model

Preferences

\[u(C_t,L_t) = \frac{C_t^{1-\sigma}}{1-\sigma} - \frac{L_t^{1+\varphi}}{1+\varphi}\]and a Cobb-Douglas production function

\[Y_t = A_t K_t^\alpha L_t^{1-\alpha}\]The model’s building blocks are

\[C_t^{\sigma} L_t^{\varphi} = W_t, \\ 1 = \beta \mathbb{E}_t\left[ \frac{C_t}{C_{t+1}} (R_{t+1} + 1 - \delta)\right], \\ R_t = \alpha \frac{Y_t}{K_t}, \\ W_t = (1-\alpha)\frac{Y_t}{L_t}, \\ Y_t = A_t K_t^\alpha L_t^{1-\alpha}, \\ K_{t+1} = (1-\delta)K_t + I_t, \\ C_t + I_t = Y_t, \\ A_t = e^{z_t}, z_{t+1} = \rho_A z_t + \varepsilon_t, \varepsilon_t ~ N(0,\sigma^2_A)\]Log-linearized version

\[0 \approx \tilde{Y}_t - \frac{\tilde{L}_t}{1-\overline{L}} - \tilde{C}_t, \\ 0 \approx \tilde{C}_t - \mathbb{E}_t \tilde{C}_{t+1} + \beta \overline{R} \mathbb{E}_t \tilde{R}_{t+1}, \\ 0 \approx \tilde{Y}_t - \tilde{K}_t - \tilde{R}_t, \\ 0 \approx z_t + \alpha \tilde{K}_t + (1-\alpha) \tilde{L}_t - \tilde{Y}_t, \\ 0 \approx \overline{Y}\tilde{Y}_t - \overline{C}\tilde{C}_t + \overline{K}[(1-\delta)\tilde{K}_t - \tilde{K}_{t+1}], \\ z_{t+1} = \rho z_t + \varepsilon_t\]where $\tilde{x}_t = \ln x_t - \ln \overline{x}$.

The steady-state variables $\overline{x}$ can be calculated either by hand or with Dynare.

Dynare codes

The following .mod can be used to solve the model

var Y I C L W R K A;

varexo e;

parameters sigma phi alpha beta delta rhoa;

sigma = 2;

phi = 1.5;

alpha = 0.33;

beta = 0.985;

delta = 0.025;

rhoa = 0.95;

model(linear);

#Rss = (1/beta)-(1-delta);

#Wss = (1-alpha)*((alpha/Rss)^(alpha/(1-alpha)));

#Yss = ((Rss/(Rss-delta*alpha))^(sigma/(sigma+phi))) *(((1-alpha)^(-phi))*((Wss)^(1+phi)))^(1/(sigma+phi));

#Kss = alpha*(Yss/Rss);

#Iss = delta*Kss;

#Css = Yss - Iss;

#Lss = (1-alpha)*(Yss/Wss);

//1-Labor supply

sigma*C + phi*L = W;

//2-Euler equation

(sigma/beta)*(C(+1)-C)=Rss*R(+1);

//3-Law of motion of capital

K = (1-delta)*K(-1)+delta*I;

//4-Production function

Y = A + alpha*K(-1) + (1-alpha)*L;

//5-Demand for capital

R = Y - K(-1);

//6-Demand for labor

W = Y - L;

//7-Equilibrium condition

Yss*Y = Css*C + Iss*I;

//8-Productivity shock

A = rhoa*A(-1) + e;

end;

//-Steady state calculation

steady;

check;

model_diagnostics;

model_info;

//-Shock simulations

shocks;

var e;

stderr 0.01;

end;

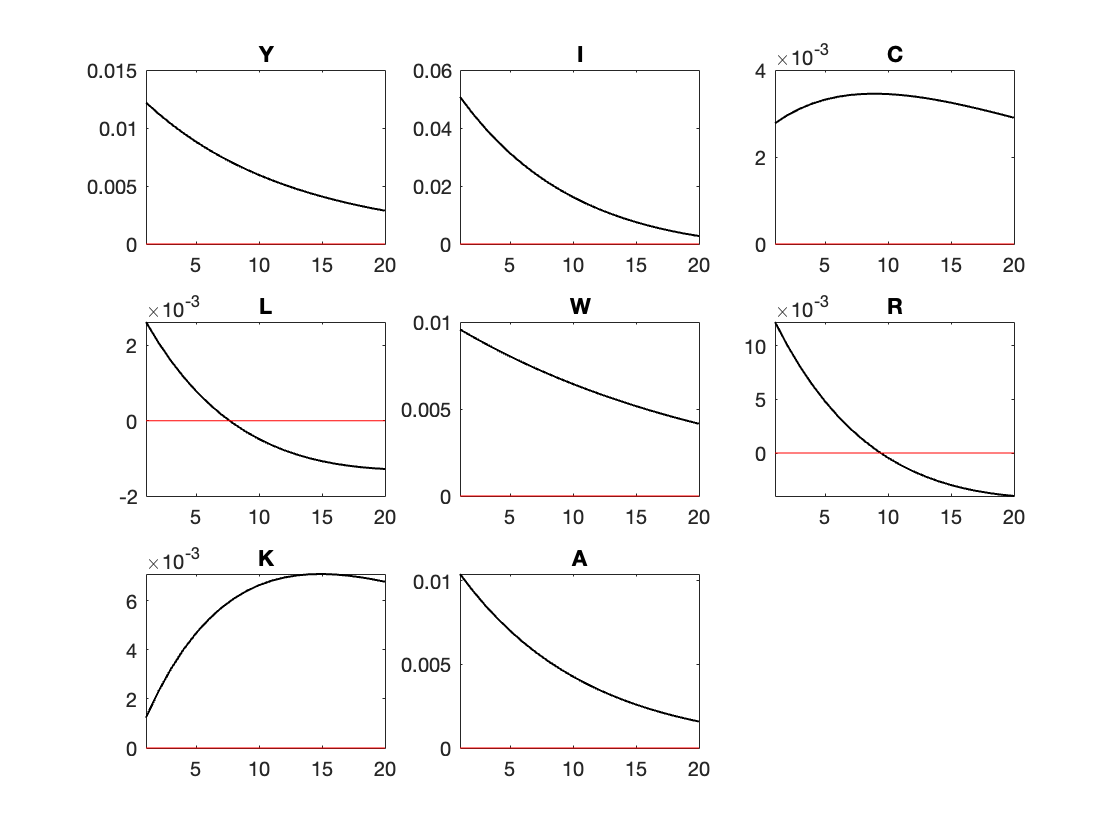

stoch_simul(order=1, irf=20) Y I C L W R K A;

The last line produces the IRF.

To extract the elements for the state-space representation, we can use the following code in MATLAB. (Please read Sims’ note)

% extract the parameters for state-space representation

% variable order: Y I C L W R K A

% state vars: 7, 8

p_Y = 1;

p_I = 2;

p_C = 3;

p_L = 4;

p_W = 5;

p_R = 6;

p_K = 7;

p_A = 8;

% create matrices for the state-space representation

% S(t) = A*S(t-1) + B*e(t)

% X(t) = C*S(t-1) + D*e(t)

A = [ oo_.dr.ghx(oo_.dr.inv_order_var(p_K),:);

oo_.dr.ghx(oo_.dr.inv_order_var(p_A),:)

];

B = [ oo_.dr.ghu(oo_.dr.inv_order_var(p_K),:);

oo_.dr.ghu(oo_.dr.inv_order_var(p_A),:)

];

C = [ oo_.dr.ghx(oo_.dr.inv_order_var(p_Y),:);

oo_.dr.ghx(oo_.dr.inv_order_var(p_I),:);

oo_.dr.ghx(oo_.dr.inv_order_var(p_C),:);

oo_.dr.ghx(oo_.dr.inv_order_var(p_R),:);

oo_.dr.ghx(oo_.dr.inv_order_var(p_W),:);

oo_.dr.ghx(oo_.dr.inv_order_var(p_L),:);

];

D = [ oo_.dr.ghu(oo_.dr.inv_order_var(p_Y),:);

oo_.dr.ghu(oo_.dr.inv_order_var(p_I),:);

oo_.dr.ghu(oo_.dr.inv_order_var(p_C),:);

oo_.dr.ghu(oo_.dr.inv_order_var(p_R),:);

oo_.dr.ghu(oo_.dr.inv_order_var(p_W),:);

oo_.dr.ghu(oo_.dr.inv_order_var(p_L),:);

];

Computing IRFs by hand

After the extraction, one can use these values to plot the IRF manually

% compute the impulse reponses by hand

sigma_e = 0.01;

% time horizon

H = 20;

Sirf = zeros(2,H);

Xirf = zeros(6,H);

Sirf(:,1) = B*sigma_e;

Xirf(:,1) = D*sigma_e;

for j = 2:H

Sirf(:, j) = A*Sirf(:, j-1);

Xirf(:, j) = C*Sirf(:, j-1);

end

%% Plotting

% Time axis

t = 1:H;

% Variable names for display (including K and A)

% variable order: Y I C L W R K A

var_names = {'Y', 'I', 'C', 'L', 'W', 'R', 'K', 'A'};

% Combine Xirf and Sirf into one matrix for plotting

IRFs_all = [Xirf; Sirf];

% Plot all IRFs

figure;

for i = 1:8

subplot(3,3,i);

plot(t, IRFs_all(i,:), 'LineWidth', 1, 'Color','black');

hold on;

yline(0, '-k', 'LineWidth', 1, 'Color','r'); % Add horizontal zero line

hold off;

title([var_names{i}]);

%xlabel('Periods');

%ylabel('Response');

%grid on;

end

sgtitle('IRFs');

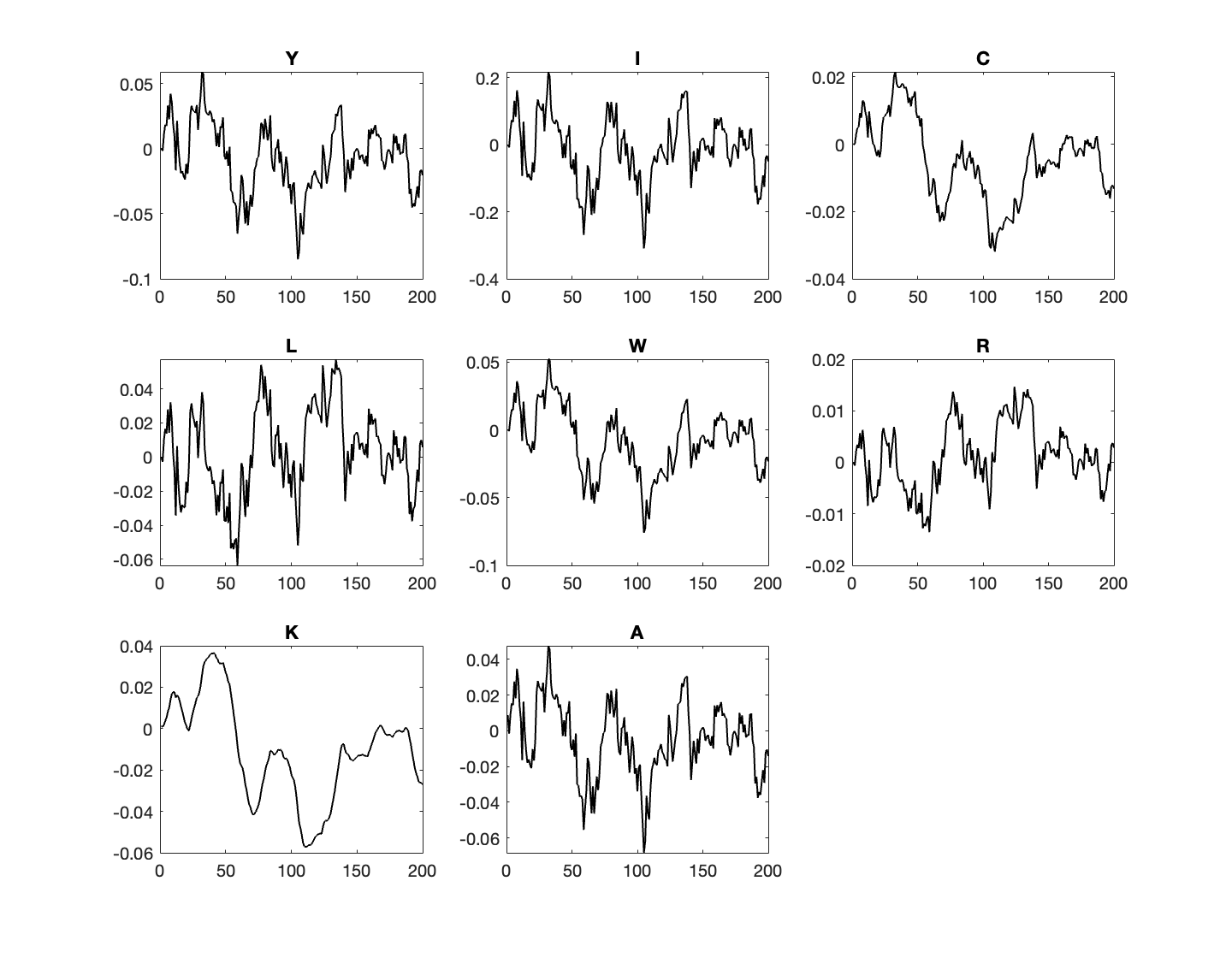

We can also generate the model’s moments based on a random series of shocks.

% compute a simulation. First draw shocks

T = 200;

e = sigma_e * randn(1,T);

Ssim = zeros(2,T);

Xsim = zeros(6,T);

% assume initial state is SS

Ssim(:,1) = B*e(1,1);

for j = 2:T

Ssim(:,j) = A*Ssim(:,j-1) + B*e(1,j);

Xsim(:,j) = C*Ssim(:,j-1) + D*e(1,j);

end

% Time axis

t = 1:T;

% Combine Xirf and Sirf into one matrix for plotting

simulated = [Xsim; Ssim];

% Plot all simulated

figure;

for i = 1:8

subplot(3,3,i);

plot(t, simulated(i,:), 'LineWidth', 1, 'Color','black');

title([var_names{i}]);

end

Model Estimation

This exercise is for demonstration only. The data and usage may contain errors.

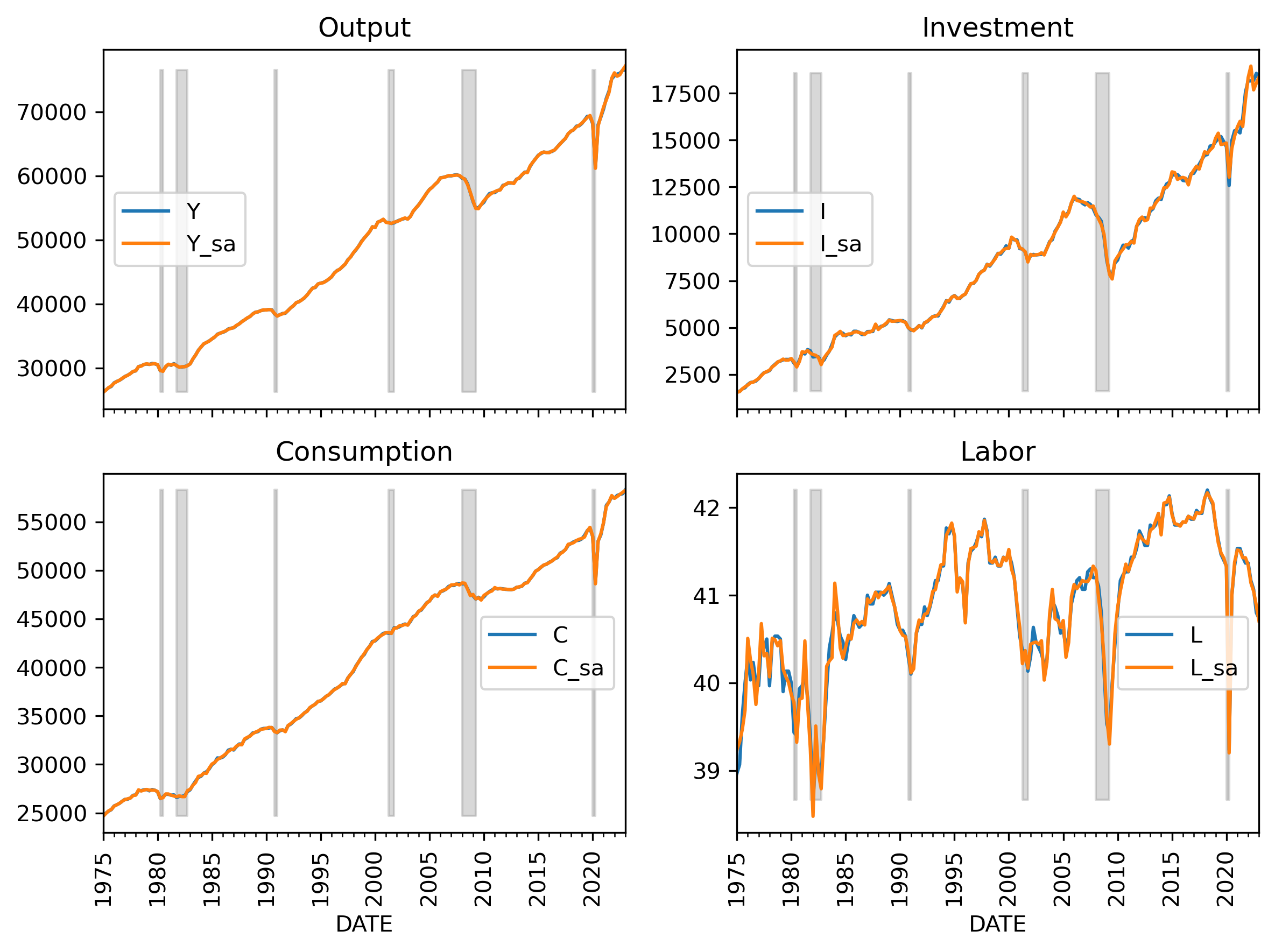

Data retrieval

First, we need some data.

For convenience, let’s use Python. The procedure is:

- Retrieve the data, calculate per-worker for Y,C,I,K,L

- Seasonally adjust all data

- Take logs and calculate the log-difference

- Then demean these values (so that we have a data matched with the model’s steady state)

# library

from pandas_datareader.data import DataReader

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from statsmodels.tsa.seasonal import STL

from statsmodels.tsa.filters.hp_filter import hpfilter

# Get some data

start='1975-01'

end = '2023-03'

labor = DataReader('HOHWMN02USQ065S', 'fred', start=start, end=end) # hours

consumption = DataReader('PCECC96', 'fred', start=start, end=end) # billions of dollars

investment = DataReader('GPDI', 'fred', start=start, end=end) # billions of dollars

capital = DataReader('NFIRSAXDCUSQ', 'fred', start=start, end=end) # million of dollars

population = DataReader('CNP16OV', 'fred', start=start, end=end) # thousands of persons

# shading for recession

recessions = DataReader('USRECQ', 'fred', start=start, end=end)

recessions = recessions.resample('QS').last()['USRECQ'].iloc[1:]

# Collect the raw values

raw = pd.concat((labor, consumption, investment, capital, population.resample('QS').mean()), axis=1)

raw.columns = ['labor', 'consumption', 'investment','capital', 'population']

raw['output'] = raw['consumption'] + raw['investment']

# convert data to units and normalize with population

y = (raw['output'] * 1e9) / (raw['population'] * 1e3)

i = (raw['investment'] * 1e9) / (raw['population'] * 1e3)

c = (raw['consumption'] * 1e9) / (raw['population'] * 1e3)

k = (raw['capital'] * 1e12)/(raw['population']*1e3)

h = raw['labor']

# assemble into 1 dataset

dta = pd.DataFrame({

'Y': y,

'I': i,

'C': c,

'L': h,

'K': k

})

# transform date to a new column with YYYYQQ format

dta['dynare_date'] = dta.index.to_period('Q').astype(str).str.replace('-', 'Q')

dta['recession'] = recessions

# Apply the STL decomposition on Y, I, C, L, K

def stl_decompose(series):

raw = series.dropna()

stl = STL(raw, period=4, robust=True)

res = stl.fit()

adjusted = raw - res.seasonal

return adjusted

# Extract the seasonally adjusted data

dta['Y_sa'] = stl_decompose(dta['Y'])

dta['I_sa'] = stl_decompose(dta['I'])

dta['C_sa'] = stl_decompose(dta['C'])

dta['L_sa'] = stl_decompose(dta['L'])

dta['K_sa'] = stl_decompose(dta['K'])

# take logs

dta['logY_sa'] = np.log(dta['Y_sa'])

dta['logI_sa'] = np.log(dta['I_sa'])

dta['logC_sa'] = np.log(dta['C_sa'])

dta['logL_sa'] = np.log(dta['L_sa'])

dta['logK_sa'] = np.log(dta['K_sa'])

# calculate the differences in logY_sa, logI_sa, logC_sa, logL_sa, logK_sa

dta['dY_sa'] = dta['logY_sa'].diff()

dta['dI_sa'] = dta['logI_sa'].diff()

dta['dC_sa'] = dta['logC_sa'].diff()

dta['dL_sa'] = dta['logL_sa'].diff()

# demean the log values

dta['dy'] = dta['dY_sa'] - dta['dY_sa'].mean()

dta['di'] = dta['dI_sa'] - dta['dI_sa'].mean()

dta['dc'] = dta['dC_sa'] - dta['dC_sa'].mean()

dta['dl'] = dta['dL_sa'] - dta['dL_sa'].mean()

# apply the Hodrick-Prescott filter to the log values

from statsmodels.tsa.filters.hp_filter import hpfilter

dta['Y_hp_cyc'], dta['Y_hp_trend'] = hpfilter(dta['logY_sa'], lamb=1600)

dta['I_hp_cyc'], dta['I_hp_tred'] = hpfilter(dta['logI_sa'], lamb=1600)

dta['C_hp_cyc'], dta['C_hp_tred'] = hpfilter(dta['logC_sa'], lamb=1600)

dta['L_hp_cyc'], dta['L_hp_tred'] = hpfilter(dta['logL_sa'], lamb=1600)

dta['K_hp_cyc'], dta['K_hp_tred'] = hpfilter(dta['logK_sa'], lamb=1600)

# calculate differences of the HP filtered values

dta['dy_hp'] = dta['Y_hp_cyc'].diff()

dta['di_hp'] = dta['I_hp_cyc'].diff()

dta['dc_hp'] = dta['C_hp_cyc'].diff()

dta['dl_hp'] = dta['L_hp_cyc'].diff()

# make sure dta'DATES is the first column

dta = dta.reset_index()

dta = dta[['DATES', 'Y', 'I', 'C', 'L', 'K', 'Y_sa', 'I_sa', 'C_sa', 'L_sa', 'K_sa',

'logY_sa', 'logI_sa', 'logC_sa', 'logL_sa', 'logK_sa',

'dY_sa', 'dI_sa', 'dC_sa', 'dL_sa',

'dy', 'di', 'dc', 'dl',

'Y_hp_cyc', 'Y_hp_trend',

'I_hp_cyc', 'I_hp_tred',

'C_hp_cyc', 'C_hp_tred',

'L_hp_cyc', 'L_hp_tred',

'K_hp_cyc', 'K_hp_tred',

'dy_hp', 'di_hp', 'dc_hp', 'dl_hp',

'recession']]

# Save the data to an excel file

# save data

dta.to_csv(usdat.csv, index=False)

Estimation

This procedure can be done in Dynare by adding two things to the .mod file.

- a measurement variable

dy(we take changes in log output as the observed data) - add one more identity equation to the

modelblock - estimate the model’s parameters using Bayesian methods

- decompose the shock from data and save it to an

xlsfile. (for estimation, burn the first 8 obs)

// ------ variable list

var Y I C L W R K A dy;

model(linear);

.

.

.

//9-measurement identity

dy = Y-Y(-1);

end;

// ---------- Observed variables ----------

varobs dy;

// ---------- Priors for Bayesian estimation ----------

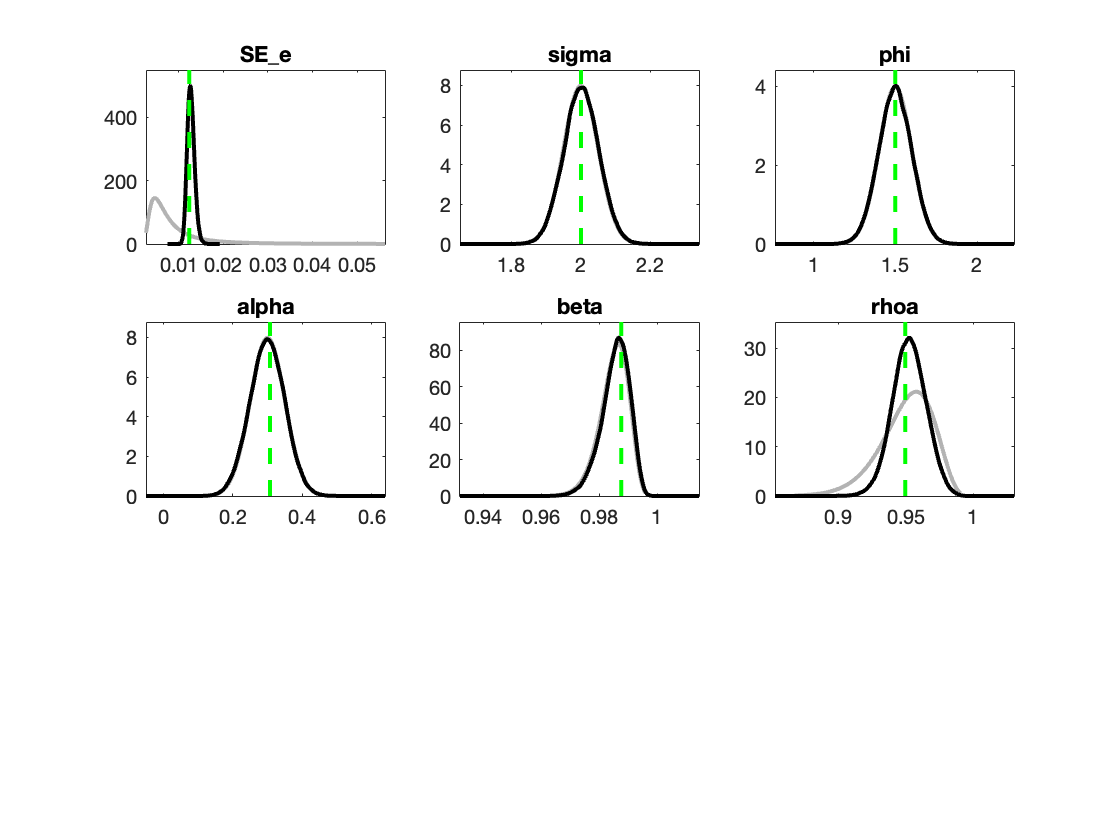

estimated_params;

sigma, 2, NORMAL_PDF, 2, 0.05;

phi, 1.5, NORMAL_PDF, 1.5, 0.1;

alpha, 0.33, NORMAL_PDF, 0.3, 0.05;

beta, 0.99, beta_pdf, 0.985, 0.005;

rhoa, 0.95, beta_pdf, 0.95, 0.02;

stderr e, 0.02, inv_gamma_pdf, 0.01, 2;

end;

// ---------- Estimation command ----------

estimation(

datafile=usdat,

first_obs=8,

presample=4,

lik_init=2,

mode_check,

prefilter=0,

mh_replic=250000,

mh_nblocks=2,

mh_jscale=1.08,

mh_drop=0.2

);

// ---------- Shock decomposition ----------

shock_decomposition(datafile=usdat, first_obs=8) dy;

plot_shock_decomposition(write_xls) dy;

| Parameter | Prior Mean | Posterior Mean | 90% HPD Interval | Prior | Std. Dev. |

|---|---|---|---|---|---|

| sigma | 2.000 | 2.0008 | [1.2735, 2.8675] | norm | 0.5000 |

| phi | 1.500 | 1.4982 | [0.9421, 1.9585] | norm | 0.3000 |

| alpha | 0.330 | 0.2986 | [0.2291, 0.3925] | beta | 0.0500 |

| beta | 0.985 | 0.9854 | [0.9775, 0.9932] | beta | 0.0050 |

| rhoa | 0.950 | 0.9523 | [0.8591, 0.9498] | beta | 0.0200 |

| e | 0.010 | 0.0127 | [0.0114, 0.0140] | invg | 2.0000 |

We can re-run the model with the Bayesian updated parameters.

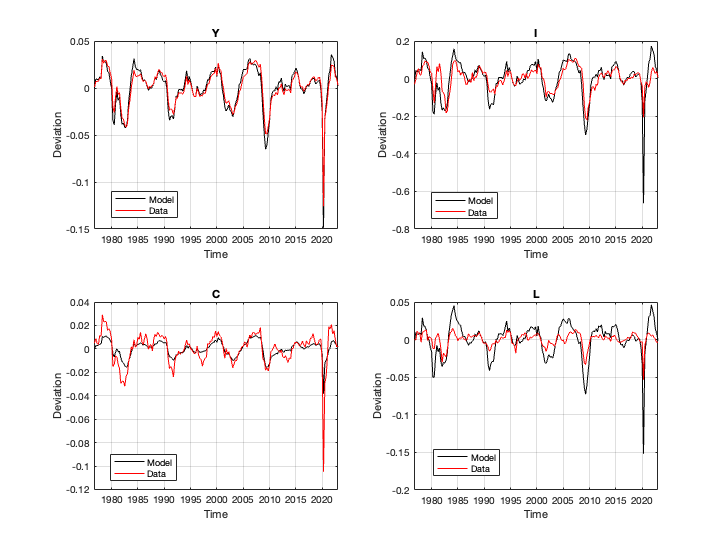

Eyeball Simulation

Aside from statistical checks, one can also simulate the model based on a given series of shocks.

Using the data from decomposition, we can produce an image like this.

The replication codes are stored here.